Menu

Performance Audits

In this section:

- Performance audit process

- What performance audits evaluate

- Choosing what to audit

- Performance audit reports and recommendations to Agency management

- Implementing recommendations and Agency accountability

Performance audits take a more in-depth look at government agency programs, activities, systems, services, processes or organizations to determine whether it achieves its intended goals and objectives in an effective, efficient, and economical manner. This assessment informs recommendations to improve overall performance by determining whether the Agency’s management, governance, and use of public resources follows good practice and complies with legislative authorities.

Performance audits span various topics and government sectors and are typically non-financial in scope. In selecting which areas to audit, we attempt to identify topics with the greatest financial, social, health, or environmental impact on Saskatchewan. See below for what do performance audits evaluate?

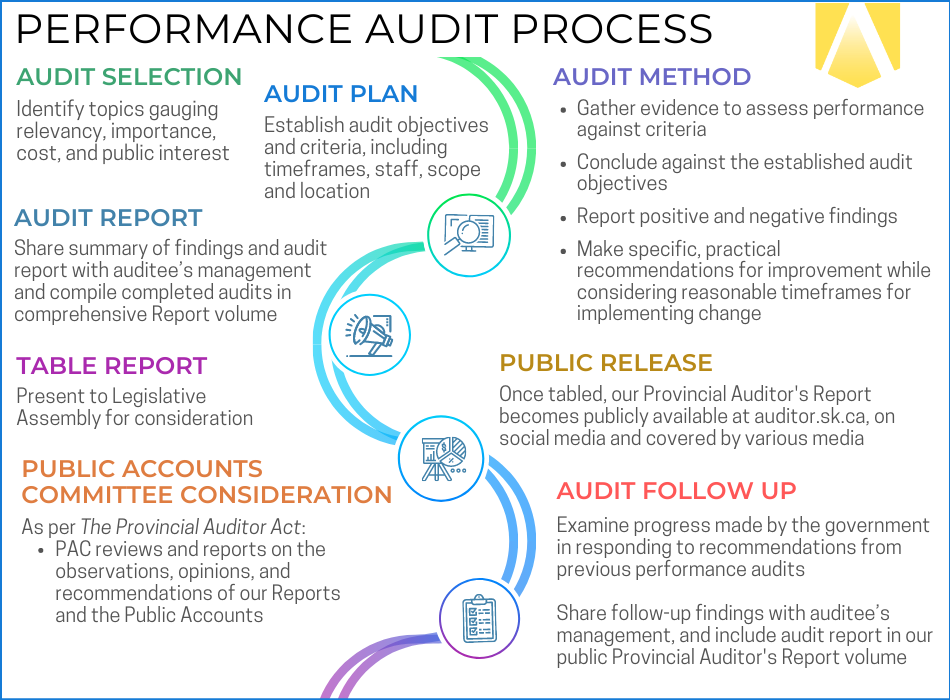

Performance Audit Process

Qualified auditors plan, perform, and report on all audits according to professional auditing standards, budgets and the Office’s policies and procedures. The Provincial Auditor and team factor in the financial and human resources required to perform a high-quality audit before undertaking a proposed audit, which includes:

- Establishing audit objectives and criteria

- Gathering evidence to assess performance against criteria

- Concluding against the established audit objectives

- Reporting positive and negative findings

- Making specific, practical recommendations for improvement

- Determining reasonable timeframes for implementing changes

- Conducting follow-up audits within reasonable timeframes

The performance audit process involves several steps, including planning, data collection, analysis, reporting, and follow up. During the planning phase, we define the scope and objective of the audit, set criteria, identify key stakeholders and risks, and develop a detailed audit plan.

Data collection involves gathering information from a variety of sources, including interviewing Agency management and/or key staff, observing processes and procedures, and reviewing documentation and records in order to form a conclusion about processes, transactions, or other information when compared to set criteria. This data analysis identifies any areas of concern or opportunities for improvement.

We evaluate the findings, discuss them with Agency management and then publish all completed audit reports in a comprehensive Provincial Auditor’s Report volume with related recommendations for performance improvement.

Finally, follow up involves monitoring the implementation of the audit recommendations and assessing whether the Agency has made improvements. We do our first follow-up either two or three years after the initial audit and every two or three years thereafter until the agency either implements the recommendations or we identify them as no longer relevant. We expect some recommendations will take government agencies a longer period to implement (e.g., five years).

What do performance audits evaluate?

Performance audits focus on specific programs or policies’ implementation, public service delivery, and can advise on best/good practice, including examining:

- Systems, processes and internal controls

- Management of public money and resources

- Results attained, as well as adequacy of performance monitoring and reporting

- Compliance with applicable laws, regulations, policies, and other legislative authorities

- Significant risks related to achieving program outcomes and safeguarding public funds

- Governance and oversight practices and effectiveness

- Impact on people and the environment

Performance audits question the government’s management practices, controls and reporting systems, but do not assess the merits of legislative policy, the adequacy of program resources, or the future state of policies and programs. For example, we would not comment on the policy direction taken by government, but could examine whether a policy is implemented appropriately.

We conduct these independent and objective assessments using professionally adopted methodologies, including auditing and assurance standards set by the Chartered Professional Accountants of Canada as outlined in the CPA Canada Handbook—Assurance. We also consult with independent specialists with subject matter expertise in particular areas to help us identify good practice and assess agency processes.

Overall, a performance audit is an important tool for improving the efficiency and effectiveness of organizations and processes, and for ensuring that public resources are used in the most effective and efficient manner possible.

How does the Office choose what to audit?

Our annual planning process includes determining potential areas of focus for future performance work. We maintain a three-year performance work plan, which we publish annually in our Business and Financial Plan [Section 4.6], highlighting potential areas of focus for performance work.

In selecting (non-financial) performance audits, the Office considers:

- Risks faced by government and government agencies

- Areas with significant social, financial, health or environmental impacts on Saskatchewan

- Areas of strategic importance to the government

- Areas of interest raised by legislators, government agencies, general public

- Topics inspired by current events and issues or public discussion

- Performance audits done by other legislative auditors

- Coverage across government

- Auditability of subject matter, including the Office’s own auditor resources and capacity to do the work

- Input of legislators, government agencies, other legislative auditors through various mechanisms

The Provincial Auditor Act gives the Provincial Auditor discretion about what areas of government to examine.

What’s in a performance audit report?

Each performance audit contains conclusions that include detailed, practical recommendations based on evidence to help government understand deficiencies and implement changes.

Performance audit reports commonly include (source: CAAF Quick Reference Performance Audit Primer):

- Audit objective(s) (the key question the audit will answer)

- A conclusion against the objective(s)

- Scope [program(s), time parameters, location(s)]

- Criteria, against which performance is assessed, derived from authoritative sources

- Findings, both positive and negative, backed up with evidence

- Recommendations to Agency management to correct identified deficiencies

Recommendations to Agency Management

When we complete an audit, the Provincial Auditor makes formal written recommendations to Agency management. A letter and a report are provided to the respective Minister and to the auditee—the leadership and management responsible for the government agency. Auditees include government ministries, Crown corporations (e.g., SaskPower), and other government agencies (e.g., Saskatchewan Health Authority, school divisions), among others. See Who Do We Audit?

We also provide auditee/Agency management with a summary of findings, and an opportunity to comment. However, we are not required to reach agreement on an audit report's content.

Provincial Auditor’s Report

Twice a year, in June and December, the Office compiles completed audit reports in two robust Provincial Auditor’s Report volumes that are released publicly once presented (tabled) at the Legislative Assembly of Saskatchewan.

The Provincial Auditor holds a press conference in advance of tabling each Report volume to inform media about key audits and results, as well as to allow media to ask clarifying questions and to interview the Provincial Auditor and/or Deputy Provincial Auditors.

Implementing Recommendations and Agency Accountability

Our recommendations to agency management aim to correct observed issues and prevent their reoccurrence. Well-designed recommendations are results-oriented, specific enough to allow for assessing progress, and practical, such that the agency can implement them in a reasonable timeframe. We expect some recommendations will take government agencies a longer period to implement (e.g., five years).

The extent to which agencies implement recommendations demonstrates whether the recommendations reflect areas that are important to improve public sector management, and whether agencies act on them quick enough. We do our first follow-up either two or three years after the initial audit and every two or three years thereafter until the agency either implements the recommendations or we identify them as no longer relevant. We include the results of our follow-up audits in our public Reports.

Quick Links

- Audit Suggestions

- Audits of Public Accounts

- Potential Performance Audit Areas

- Social Media Terms of Use

- Senior Management Travel Expenses

- Frequently Asked Questions