Menu

Types of Audits

Our Work and Audit Plans

As part of our annual business and financial planning process, the Office prepares an annual work plan that covers all government agencies. Because the Legislative Assembly, Cabinet, and government agencies create or wind-up other government agencies, we monitor their actions and continually update our list of government agencies. We estimate the costs of carrying out our work plan and ask the Assembly for the money to carry out the plan.

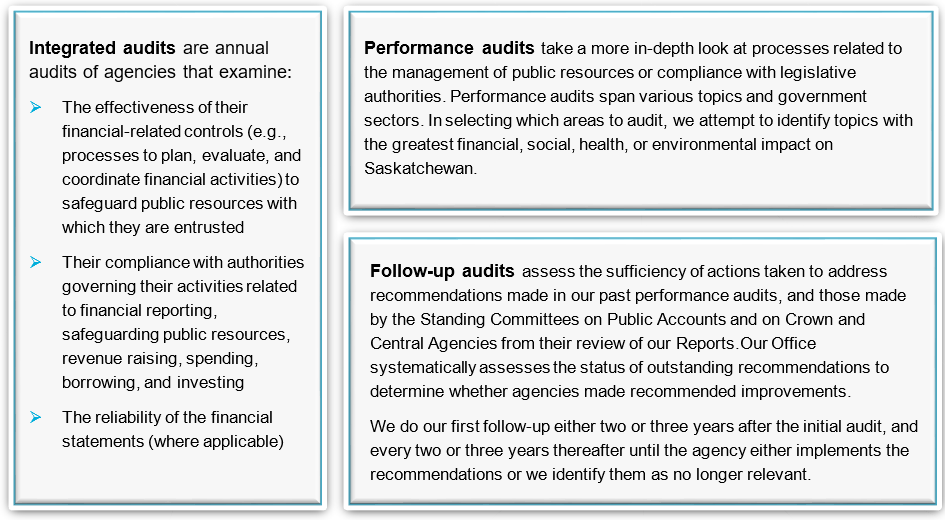

To carry out our work plan, we perform three types of audits:

Our annual planning process includes determining potential areas of focus for future performance audit work. We include a three-year performance work plan in Section 4.6 of our business and financial plan each year. See our future performance audit areas. Performance audits question the government’s management practices, controls and reporting systems. Learn more about performance audits and our process to conduct this type of audit work.

Learn more about Who We Audit

Conducting Relevant Work

The Office’s strategic plan provides a foundation for developing the Office’s annual business and financial plans provided to the Public Accounts Committee.

Planning processes seek external input to help direct our efforts toward relevant issues. These processes include identifying external forces, emerging trends, and risks facing the Government and the Office; and assessing their impact on the Office and our plans. How the Government manages its risks affects the nature and extent of the Office’s work.

The Office uses surveys to assess the satisfaction of agencies we audit. We also continuously seek advice from stakeholders when we work with appointed auditors.

The Office uses a risk-based model to focus our work. We focus our efforts on helping our stakeholders address the challenges and opportunities emerging from external forces and trends.

The reporting processes include reporting the Office’s assurance and advice directly to the Legislative Assembly and the Government. Our Reports contain the matters that, in the Office’s view, are significant to the Assembly and the public.

Before submitting our Report volumes to the Assembly, the Office prepares and discusses the results of each audit with the applicable agency. This includes meeting with agencies to confirm the findings and gain support for our recommendations. When deciding what to report, the Office considers whether the matter:

- Affects the Assembly’s ability to control the financial activities of the Government or to hold the Government accountable for how it administers public money

- Involves improving how the Government administers public money or its compliance with legislative authorities

- Involves non-compliance with legislative authorities

At the end of each audit, the Office issues a final report to the Minister responsible, senior officials of the agency and, if applicable, the Chair of the agency’s governing body (e.g., Board) with a copy to the Chair and Secretary of the Treasury Board and to the Provincial Comptroller.

Provincial Auditor's Report

Twice a year, in June and December, the Office compiles completed audit reports in two robust Report volumes that are released publicly once presented (tabled) at the Legislative Assembly of Saskatchewan.

Quick Links

- Audit Suggestions

- Audits of Public Accounts

- Potential Performance Audit Areas

- Social Media Terms of Use

- Senior Management Travel Expenses

- Frequently Asked Questions