Menu

2022 Report Volume 2

Our 2022 Report – Volume 2 includes the results of five non-financial performance audits, 13 follow-up audits, and annual integrated audits of 163 different agencies with year-ends between January and June 2022. These audits are conducted by our Office or along with appointed auditors (if in place) and include integrated audits of 19 ministries, 100 Crown corporations and agencies, eight pension and employee benefit plans, and 36 healthcare affiliates. Appendix 1 lists each agency along with its year-end date, whether matters are reported, and, if so, in which Report.

Annual Integrated Audits' Highlights

This section includes concerns at only six government agencies, which means most agencies had effective financial-related controls, complied with financial and governance-related legislative authorities, and prepared reliable financial statements.

The Ministry of Social Services (Chapter 6) has further work to do to make sure its clients are paid correct income assistance amounts under the Saskatchewan Income Support (SIS) Program. Verifying client income and educating Ministry staff on payment and overpayment recovery requirements should support clients getting the correct income assistance amounts from SIS.

eHealth Saskatchewan (Chapter 1) continued to make progress on testing its IT disaster recovery plans but did not fully complete testing. Fully testing recovery plans assures key IT systems that support critical healthcare services can be successfully restored within a reasonable time when disasters occur (e.g., cyberattacks).

As Chapter 3 reports, the Prairie Agricultural Machine Institute (PAMI) did not prepare adequate financial statements for audit in 2021–22 and did not table its March 31, 2022 financial statements in accordance with legislative requirements. PAMI management had to correct significant errors in the financial statements; PAMI’s final audited financial statements are reliable. PAMI requires effective controls to accurately track revenue from its fee-for-service projects, and review and approve financial information once prepared.

The Saskatchewan Liquor and Gaming Authority (Chapter 5) had an adequate policy for protecting credit card information but did not follow it. The Authority inappropriately stored about 125 credit card numbers of liquor retailers and regulatory clients on its network. Not following its policy can result in loss of sensitive information.

Performance Audits

Performance audits take a more in-depth look at processes related to the management of public resources or compliance with legislative authorities. Performance audits span various topics and government sectors. In selecting which areas to audit, we attempt to identify topics with the greatest financial, social, health, or environmental impact on Saskatchewan. Three highlighted performance audits 'At a Glance' are as follows:

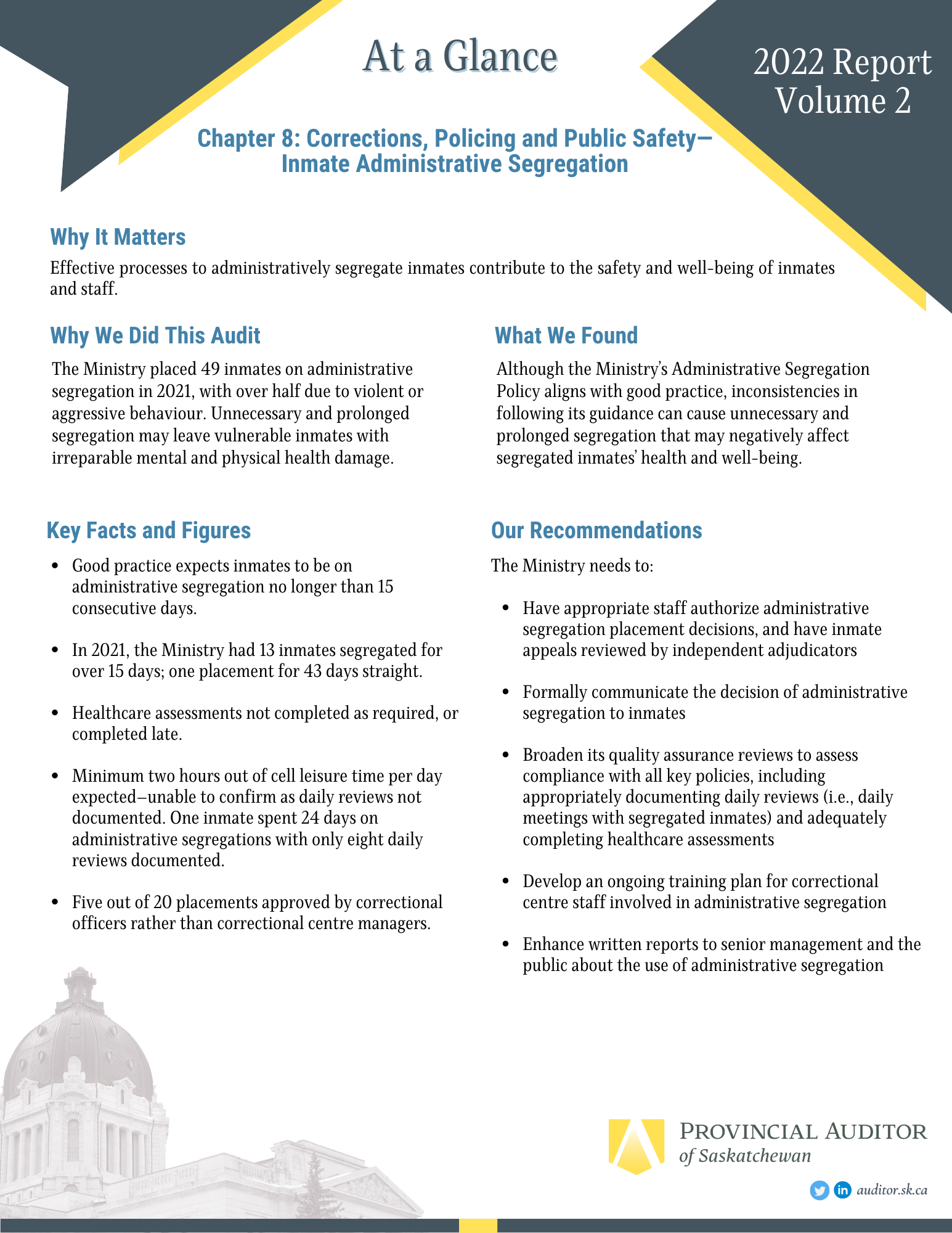

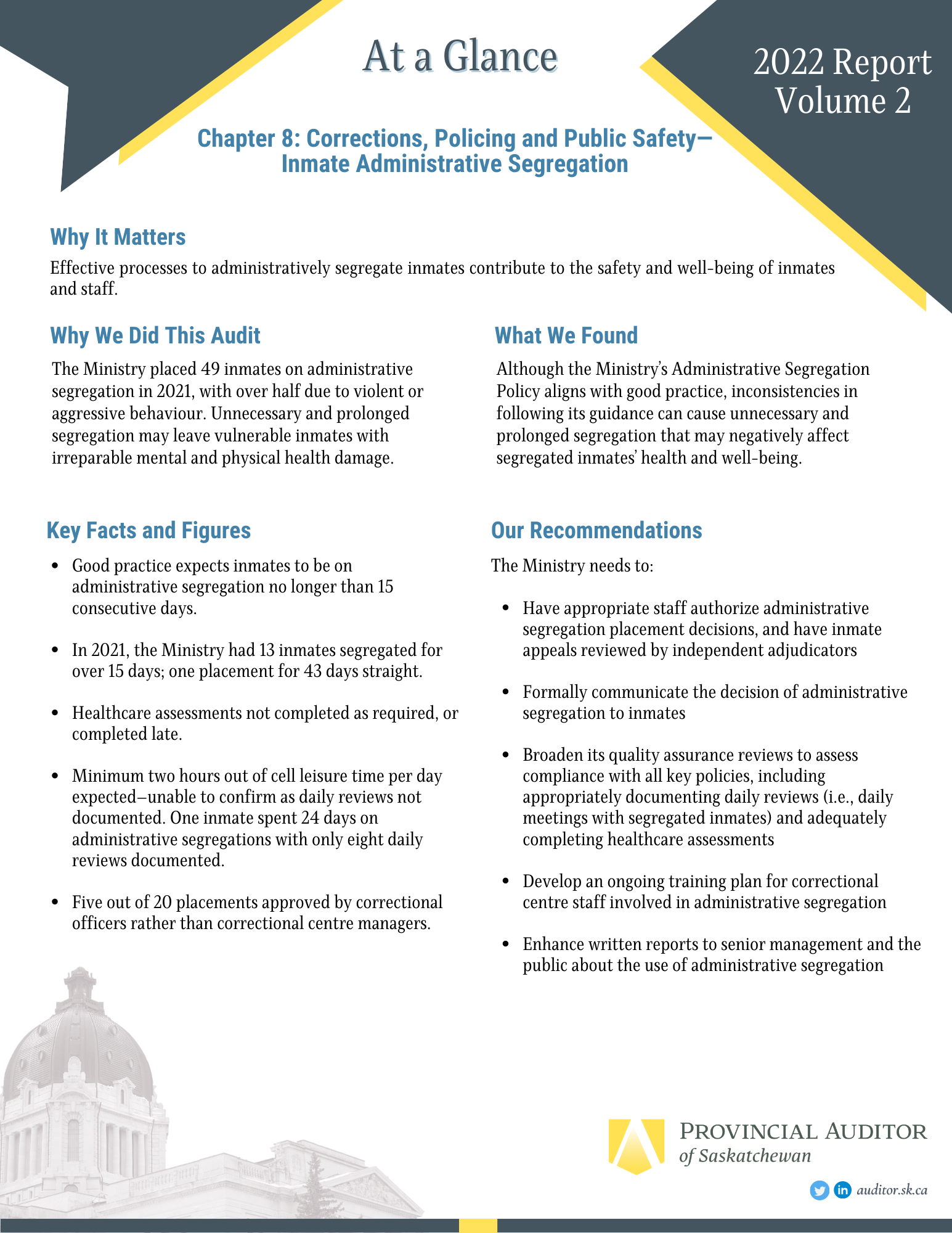

Chapter 8 'At a Glance' Analyzing Inmate Administrative Segregation

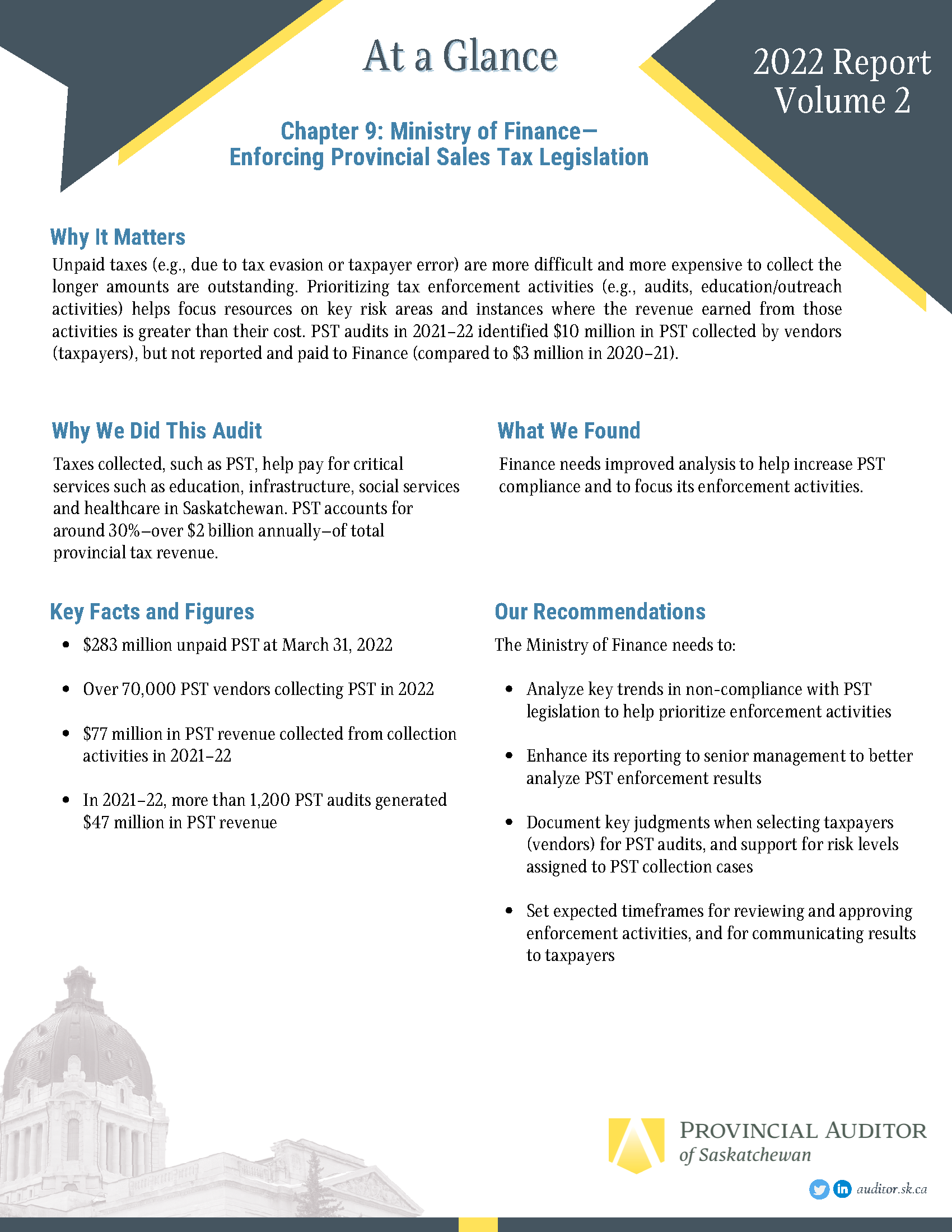

Chapter 9 'At a Glance' Enforcing Provincial Sales Tax Legislation

Chapter 12 'At a Glance' Filling Hard-to-Recruit Healthcare Positions

{kind=link}

Follow-Up Audits

Overall, agencies implemented more recommendations on an overall basis (59%) than our recent Report (2022 Report – Volume 1: 42%). The percentage of recommendations not implemented (at 6%) is also lower compared to our past Report (2022 Report – Volume 1: 18%).

The extent to which agencies implement recommendations demonstrates whether the recommendations reflect areas that are important to improve public sector management, and whether agencies act on them quick enough. We are happy to see agencies acting on our recommendations in a timelier manner, as this means public sector management is improving.

Some agencies were successful in making improvements in a relatively short period. For example, Saskatchewan Polytechnic (Chapter 22) improved its processes to carry out applied research. Sask Polytech earns revenue by providing applied research to governments, corporations, and other third parties. Sask Polytech developed a new database to centralize and track research projects, expanded its measures to assess the success of its applied research, and established written agreements with industry partners requiring research projects.

Further work is needed at some agencies.

As noted in Chapter 20, the Saskatchewan Health Authority has more work to do to maintain healthcare facilities in Saskatoon and surrounding areas. Overall, facilities in Saskatoon and surrounding areas are in critical condition, and worsening. The Authority still has to set measurable service objectives to assist in determining which facilities and components are in immediate need of maintenance. Having minimum condition standards enables taking a risk-informed approach to maintenance planning. Further, the Authority is not conducting preventative maintenance activities on a consistent basis or appropriately prioritizing on-demand maintenance requests. This not only increases the risk that key facilities and components remain unrepaired longer than they should, but also that an asset may fail and cause harm to residents, patients, visitors, or staff.

As noted in Chapter 15, eHealth Saskatchewan still has to implement adequate configuration settings on all eHealth-managed portable computing devices to prevent exposing the eHealth IT network to viruses and malware. Portable computing devices, like laptops, create paths to IT networks. Sufficiently controlling and monitoring eHealth’s IT network will also help to mitigate the impact of security breaches.

Media Materials 2022 Report – Volume 2

- News Release 2022 Report – Volume 2: Enforcing Provincial Sales Tax Legislation

- News Release 2022 Report – Volume 2: Inmate Administrative Segregation

- News Release 2022 Report – Volume 2: Filling Hard-to-Recruit Healthcare Positions

- 2022 Report – Volume 2: Backgrounder

- Compilation of Main Points/Executive Summary

- Download the Full Report

(For selective viewing please click on an individual chapter from the list below)

Provincial Auditor of Saskatchewan's Overview

Tara Clemett's Complete Overview 2022 Report – Volume 2

Our Office’s mission to promote accountability and better management of public resources, while preserving our independence, provides legislators and the public with an independent assessment of the Government’s use of public resources. We do this through our audit work and publicly reported results, along with our mutual involvement with legislative committees charged with reviewing our Reports.

This 2022 Report – Volume 2 provides legislators and the public critical information on whether the Government issued reliable financial statements, used effective processes to administer programs and services, and complied with governing authorities. It includes the results of examinations of different agencies completed by November 4, 2022 with details on annual integrated and performance audits, as well as our follow-up audit work on previously issued recommendations by our Office and by the Standing Committees on Public Accounts and Crown and Central Agencies.

Table of Contents

2022 Report – Volume 2 Table of Contents

Annual Integrated Audits

3 Prairie Agricultural Machinery Institute

4 Saskatchewan Health Authority

5 Saskatchewan Liquor and Gaming Authority

7 Summary of Implemented Recommendations

Performance Audits

8 Corrections, Policing and Public Safety—Inmate Administrative Segregation

9 Finance—Enforcing Provincial Sales Tax Legislation

10 Saskatchewan Cancer Agency—Cancer Drug Supply Management

11 Saskatchewan Government Insurance—Licensing Commercial Drivers

12 Saskatchewan Health Authority—Filling Hard-to-Recruit Healthcare Positions

Follow-Up Audits

13 Corrections, Policing and Public Safety—Community Rehabilitation of Adult Offenders

15 eHealth Saskatchewan—Securing Portable Computing Devices

16 Environment—Sustainable Fish Population Management

17 Finance—Monitoring the Fuel Tax Exemption Program

18 Parks, Culture and Sport—Providing Safe Drinking Water in Provincial Parks

19 Saskatchewan Health Authority—Analyzing Surgical Biopsies in Regina and Saskatoon Labs

21 Saskatchewan Impaired Driver Treatment Centre—Delivering the Impaired Driver Treatment Program

22 Saskatchewan Polytechnic—Carrying Out Applied Research

23 Saskatchewan Public Safety Agency—Coordinating Provincial Emergency Preparedness

24 Social Services—Minimizing Employee Absenteeism

25 Western Development Museum—Permanently Removing Historical Artifacts

Standing Committees

26 Standing Committee on Crown and Central Agencies

27 Standing Committee on Public Accounts

Appendices

1-1 Agencies Subject to Examination Under The Provincial Auditor Act and Status of Audits

2-1 Report on the Financial Statements of Agencies Audited by Appointed Auditors

All Prior Reports

All prior reports are available here for your reference.

Acknowledgements

Our Office continuously values the cooperation from the staff and management of government agencies, along with their appointed auditors, in the completion of the work included in this Report. We are grateful to the many experts who shared their knowledge and advice during the course of our work.

We also appreciate the ongoing support of the all-party Standing Committees on Public Accounts and on Crown and Central Agencies, and acknowledge their commitment in helping to hold the Government to account. Our Office remains focused on serving the Legislative Assembly and the people of Saskatchewan.

As Provincial Auditor, I am honoured to lead the Office, and our team of professionals. I am truly proud of their diligence and commitment to quality work. Our team’s steadfast professionalism helps us fulfill our mission—to promote accountability and better management by providing legislators and Saskatchewan residents with an independent assessment of the Government’s use of public resources.

Quick Links

- Audit Suggestions

- Audits of Public Accounts

- Potential Performance Audit Areas

- Social Media Terms of Use

- Senior Management Travel Expenses

- Frequently Asked Questions