Menu

2024 Report Volume 2

December 3, 2024

December 3, 2024

2024 Report – Volume 2

This 2024 Report – Volume 2 delivers legislators and the public critical information on whether the Government issued reliable financial statements, used effective processes to administer programs and services, and complied with governing authorities. It includes the results of audit examinations of different agencies completed by November 4, 2024, with details on annual integrated (financial) and performance audits, as well as our follow-up audit work on previously issued recommendations by our Office and agreed to by the Standing Committees on Public Accounts or on Crown and Central Agencies.

Annual Integrated Audits

Since our 2024 Report – Volume 1, our Office, along with appointed auditors (if in place), completed annual integrated audits of 175 different agencies with fiscal year-ends between January 2024 and July 2024. These include integrated audits of 17 ministries, 33 Crown corporations and agencies, seven pension and employee benefit plans, and 36 healthcare affiliates.

This section includes concerns at 10 agencies, which means most agencies had effective financial-related controls, complied with financial and governance-related legislative authorities, and prepared reliable financial statements.

eHealth Saskatchewan (Chapter 1) has yet to sufficiently test its disaster recovery plans to ensure it can restore critical IT systems it manages for the health sector. Without tested plans, eHealth, as well as the Saskatchewan Health Authority, Saskatchewan Cancer Agency, and the Ministry of Health may not be able to deliver time-sensitive health services in the event of disaster.

There are certain government agencies lacking adequate review and approval of financial information, such as bank reconciliations, revenue reconciliations, and journal entries increasing the risk of errors in financial information and misappropriation of public funds. We found these concerns at Government Relations’ Northern Municipal Trust Account (Chapter 3), Ministry of Highways (Chapter 5), Northlands College (Chapter 6), Prairie Agricultural Machinery Institute (Chapter 7), and Western Development Museum (Chapter 10).

Further, Social Services (Chapter 9) did not consider best value when procuring appropriate hotel rooms for its clients prior to March 2024. Since March 2024, Social Services began two hotel pilot projects. It began obtaining three quotes when procuring hotel rooms as well as contracted two hotels (one in Saskatoon and one in Regina) to secure hotel rooms at fixed rates for the next year. Social Services needs to centrally collect reliable data related to these pilots so it can conduct a robust evaluation and determine whether these pilots resulted in efficiency and effectiveness improvements. Social Services also needs to publicly disclose payments made to vendors (e.g., hotels) on behalf of its clients to increase transparency and accountability. Moreover, it needs to demonstrate it considered best value when procuring hotel rooms for its child and family program clients—we found instances where Ministry staff may not have selected the hotel with the lowest nightly rate and did not document why not.

Performance Audits

Performance audits take a more in-depth look at processes related to the management of public resources or compliance with legislative authorities. Performance audits span various topics and government sectors. In selecting which areas to audit, we attempt to identify topics with the greatest financial, social, health, or environmental impact on Saskatchewan. This Report includes the results of four non-financial, performance audits. Two highlighted performance audits 'At a Glance' are as follows:

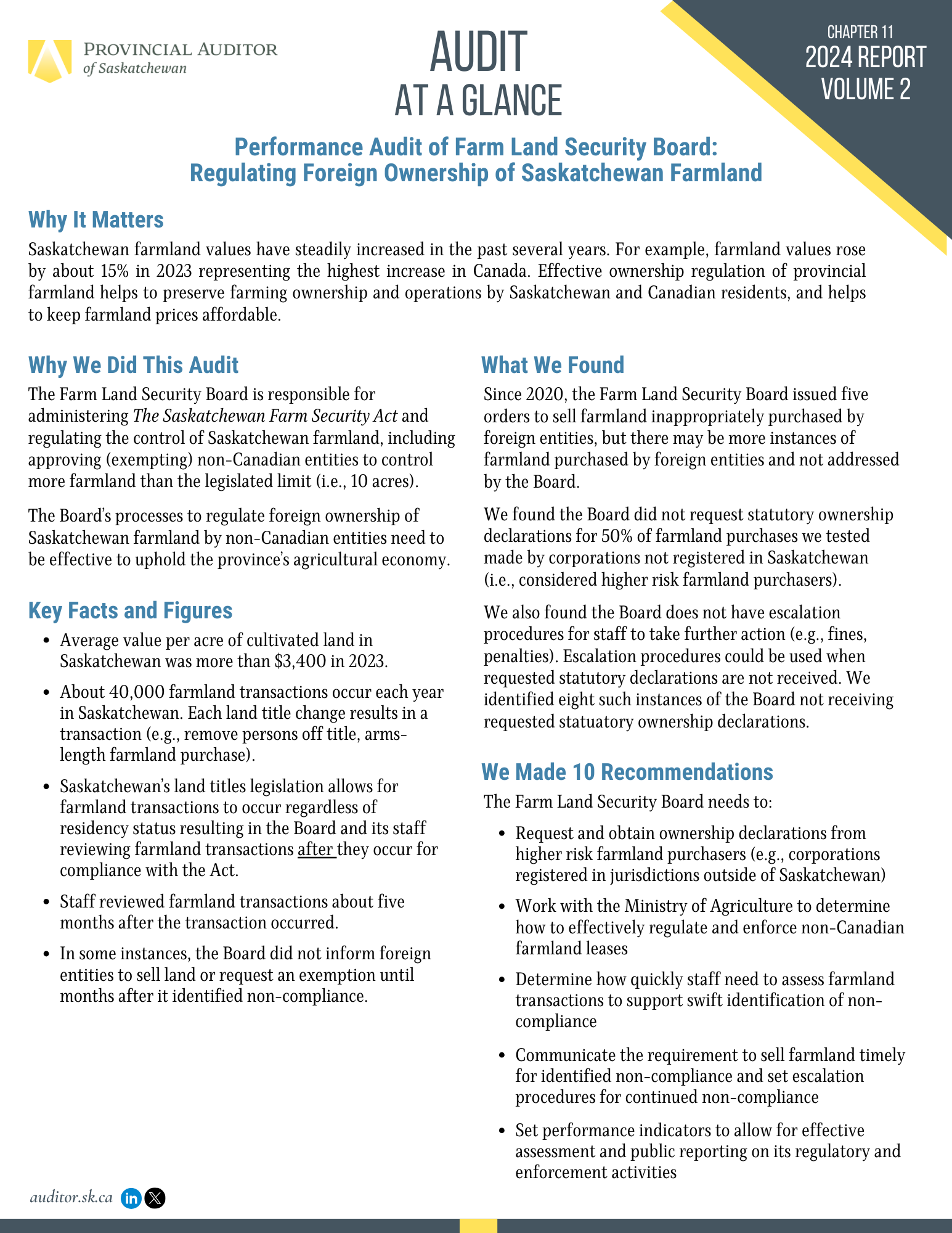

Audit At a Glance Farm Land Security Board—Regulating Foreign Ownership of Saskatchewan Farmland

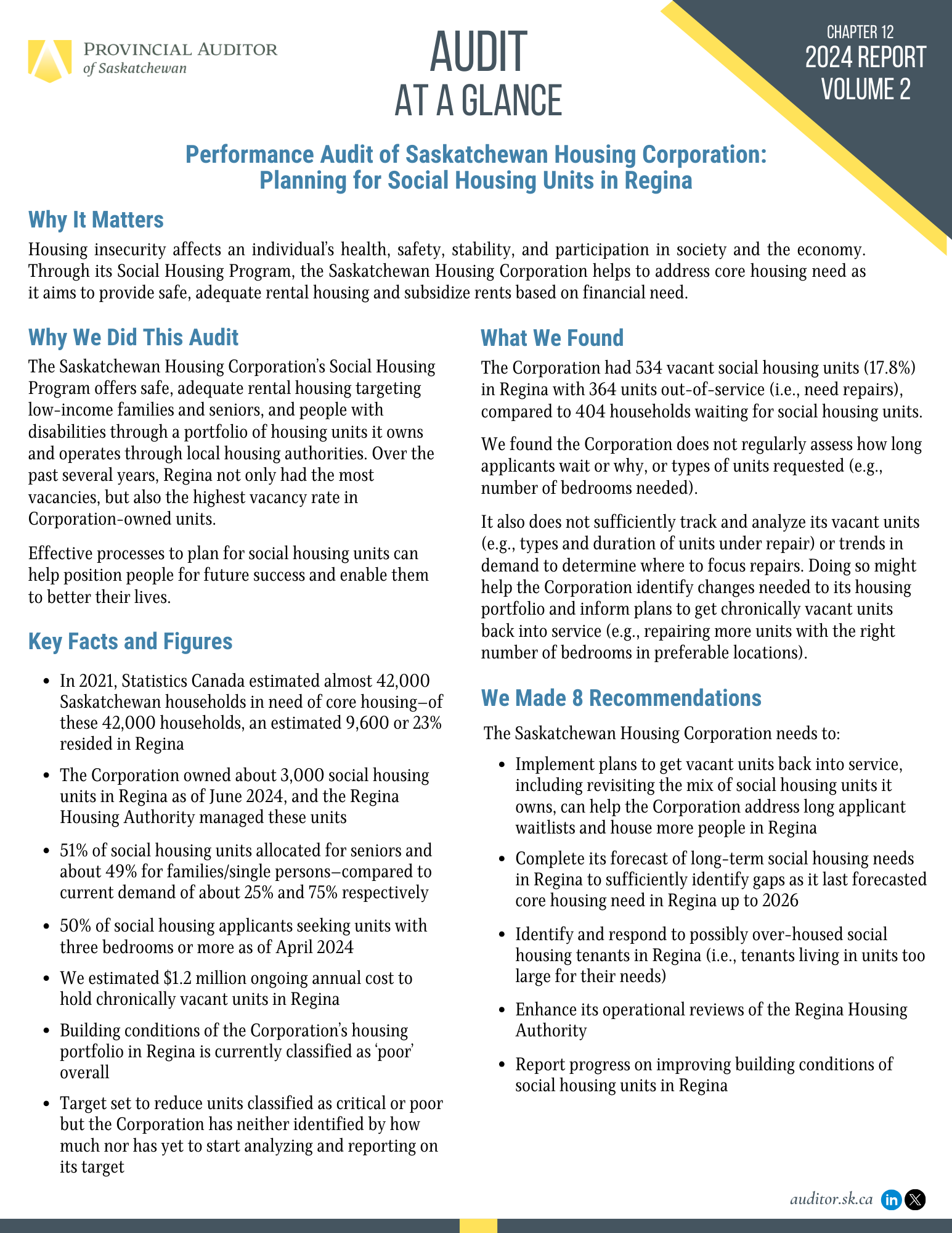

Audit At a Glance Saskatchewan Housing Corporation—Planning for Social Housing Units in Regina

Follow-up Audits

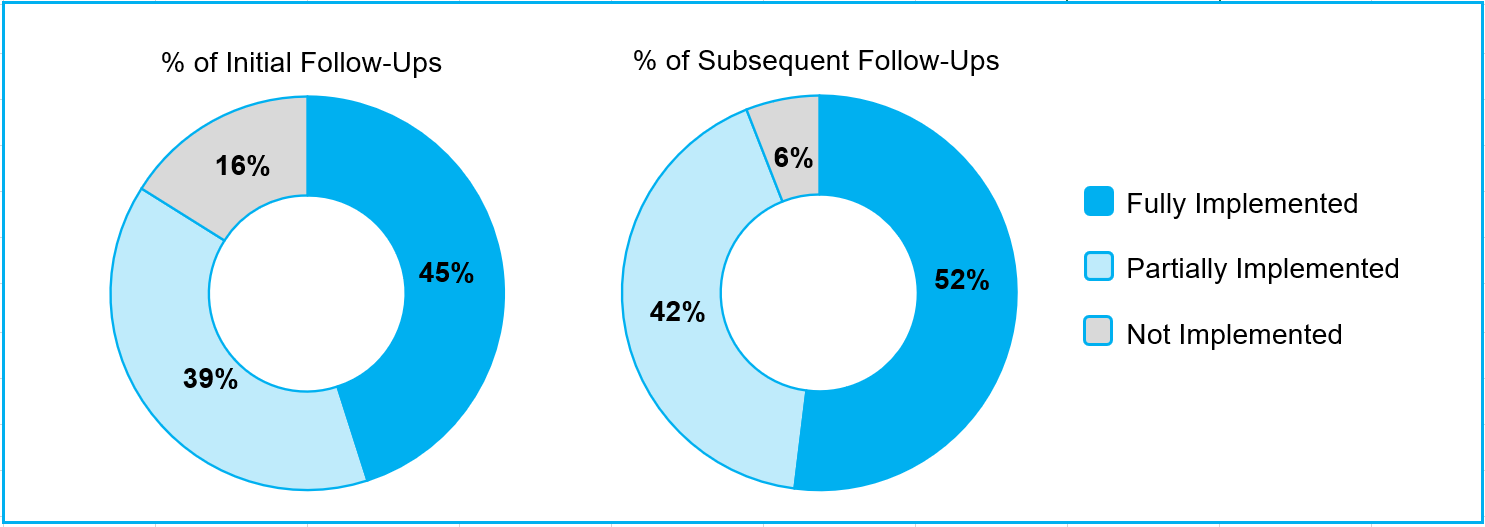

The Report highlights the results of 17 follow-up audits, as well as summarizes how quickly government agencies addressed our recommendations and made process improvements. The extent to which agencies implement recommendations demonstrates whether the recommendations reflect areas that are important to improve public sector management, and whether agencies act on them quick enough.

As shown in the Figure below, 45% of the audit recommendations in this Report were fully implemented after the initial follow-up (i.e., 2–3 years after original audit) at the various agencies. For agencies with subsequent follow-ups (i.e., >3 years after original audit) in this Report, 52% of audit recommendations have been fully implemented. We are pleased to see some agencies are acting on our recommendations in a timely manner, as this means public sector management is improving.

Some agencies like the Saskatchewan Cancer Agency (Chapter 25) made process improvements in a relatively short timeframe having implemented all five recommendations we made in our 2022 audit of its processes to manage its supply of cancer drugs.

However, further work is needed at some agencies.

The Ministry of Health (Chapter 20) is responsible for overseeing critical incident reporting in the healthcare sector. The Ministry receives critical incident reports from healthcare organizations like the Saskatchewan Health Authority and needs to sufficiently assess planned corrective actions to help ensure they effectively address causes of critical incidents. The Ministry continues to receive critical incident reports later than required by law and does not sufficiently enforce compliance. The Ministry must also effectively determine when to issue patient safety alerts to help implement system-wide improvements, otherwise the degree of injury and types of critical incidents that occur in Saskatchewan healthcare facilities will not reduce over time.

The Ministry of Social Services (Chapter 31) licensed about 280 group homes and 180 private service homes in Saskatchewan providing accommodations, meals, and care to adult clients with intellectual disabilities at April 2024. The Ministry had yet to update its inspection checklist for approved private service homes and continued to not inspect each group home annually. Also, the Ministry has yet to verify completion of periodic criminal record checks for staff working at group and approved private service homes and it lacked regular contact with clients. The Ministry still needs to analyze serious incident reports to identify homes with critical concerns and follow up with home operators on the implementation of recommendations from serious incident reports. This will support adults with intellectual disabilities to live fulfilling lives, free from safety and health threats.

We found both Northern Lights School Division (Chapter 22) and Northlands College (Chapter 23) need to strengthen their processes to purchase goods and services to support transparency, fairness, and achievement of best value. This includes documenting justification for sole source purchases, approving contracts and purchases before receiving goods or services, segregating incompatible purchasing duties, and reconciling fleet card statements prior to making payments.

Additionally, we made one new recommendation during our follow-up audit about purchasing processes at Northlands College related to the College’s non-compliance with its established policies for travel expense claims and corporate credit cards. For example, we found two instances where a corporate credit card was used for personal reasons and we found senior management incurred travel expenses without adequate support or prior approval, including an international trip costing the College roughly $19,000. Lack of adequate support and approval increases the risk of inappropriate or fraudulent purchases by staff.

Media Materials 2024 Report – Volume 2

- Compilation of All Audits' Main Points/Executive Summaries

- 2024 Report V2: Planning for Social Housing in Regina NEWS RELEASE

- 2024 Report V2: Regulating Foreign Ownership of Saskatchewan Farmland NEWS RELEASE

- 2024 V2: BACKGROUNDER

Full 2024 V2 Report

Provincial Auditor of Saskatchewan's Overview

Tara Clemett's Complete Overview 2024 Report – Volume 2

Table of Contents

2024 Report – Volume 2 Table of Contents

Annual Integrated Audits

3 Government Relations—Northern Municipal Trust Account

5 Highways

7 Prairie Agricultural Machinery Institute

8 Saskatchewan Health Authority

Performance Audits

11 Farm Land Security Board—Regulating Foreign Ownership of Saskatchewan Farmland

12 Saskatchewan Housing Corporation—Planning for Social Housing Units in Regina

13 Saskatchewan Public Safety Agency—911 Call Taking and Dispatching for Fire Emergencies

14 SaskPower—Transitioning to Low and Non-Emitting Energy Sources

Follow-Up Audits

15 Corrections, Policing and Public Safety—Inmate Segregation

16 Corrections, Policing and Public Safety—Rehabilitating Adult Inmates

17 eHealth Saskatchewan—Securing Portable Computing Devices

18 Finance—Monitoring the Fuel Tax Exemption Program

19 Health—Preventing Diabetes-Related Health Complications

20 Health—Using Critical Incident Reporting to Improve Patient Safety

21 Immigration and Career Training—Coordinating English-language Programs

22 Northern Lights School Division No. 113—Purchasing Goods and Services

23 Northlands College—Purchasing Goods and Services

24 Saskatchewan Arts Board—Awarding Grants Impartially and Transparently

25 Saskatchewan Cancer Agency—Cancer Drug Supply Management

26 Saskatchewan Health Authority—Analyzing Surgical Biopsies in Regina and Saskatoon Labs

27 Saskatchewan Health Authority—Efficient Use of MRIs in Regina

28 Saskatchewan Legal Aid Commission—Providing Legal Aid Services

29 Saskatchewan Liquor and Gaming Authority—Regulating Commercial Permittees’ On-Table Sale of Liquor

30 SaskPower—Maintaining Above-Ground Assets Used to Distribute Electricity

31 Social Services—Monitoring Quality of Care in Homes Supporting Adults with Intellectual Disabilities

Standing Committees

32 Standing Committee on Crown and Central Agencies

33 Standing Committee on Public Accounts

Appendices

1-1 Agencies Subject to Examination under The Provincial Auditor Act and Status of Audits

2-1 Report on the Financial Statements of Agencies Audited by Appointed Auditors

All Prior Reports

All prior reports are available here for your reference.

Acknowledgments

Our Office continuously values the cooperation from the staff and management of government agencies, along with their appointed auditors, in the completion of the work included in this Report. We appreciate the many experts who shared their knowledge and advice during the course of our work.

We also appreciate the ongoing support of the all-party Standing Committees on Public Accounts and on Crown and Central Agencies, and acknowledge their commitment in helping to hold the Government to account. Our Office remains focused on serving the Legislative Assembly and the people of Saskatchewan; we are committed to making a difference for a sustainable Saskatchewan and its people.

Quick Links

- Audit Suggestions

- Latest Report

- Senior Management Travel Expenses

- Potential Performance Audit Areas

- Social Media Terms of Use